Holiday Gig(s) to Millionaire

Seem like a Stretch? It is not.

You finally got a call (or email) and accepted your first gig! Usually, for us musicians it is a Christmas, Easter, a Wedding, or a Caroling gig of some sort. At the end of the memorable night you make a few hundred dollars and feel the satisfaction that comes from making money performing your craft for others!

Now what? Spend it? Go out to a fancy dinner? Buy even more Christmas Gifts no one really needs?

Nope. None of these are going to make you a millionaire… But what if you invest it? Lets take a quick look!

First Let me ask you a question.

Would it be possible for you to save $20 a week? or $83 a month to be exact? If you have a regular job at Starbucks, Teaching, or in Retail, you can likely save $20 a week/paycheck automatically an alternative to gig income.

Lets say you are 21 years old and have just graduated college and have started getting some calls for holiday gigs. Great!

Yearly Gig Income;

Christmas Eve & Morning – $400

Easter Morning – $400

Birthday Gift, Wedding Gig(s), Graduation Gig etc. – $200

Grand total of $1000 earned

Invest this in your ROTH IRA with an index fund like Vanguard’s S&P 500 fund “VFIAX”. The estimated return for this well-diversified and stable fund is 10% since 1957. (Click here for that data)

How much money do you think you would have? Take a second and think about it. $1000 a year x 40 years = $40,000! Wait, thats not a million dollars you say! Well, that is because putting it underneath your bed in a shoe box does not put your dollars to work for you in the market!

The alternative, invest it and let it compound!

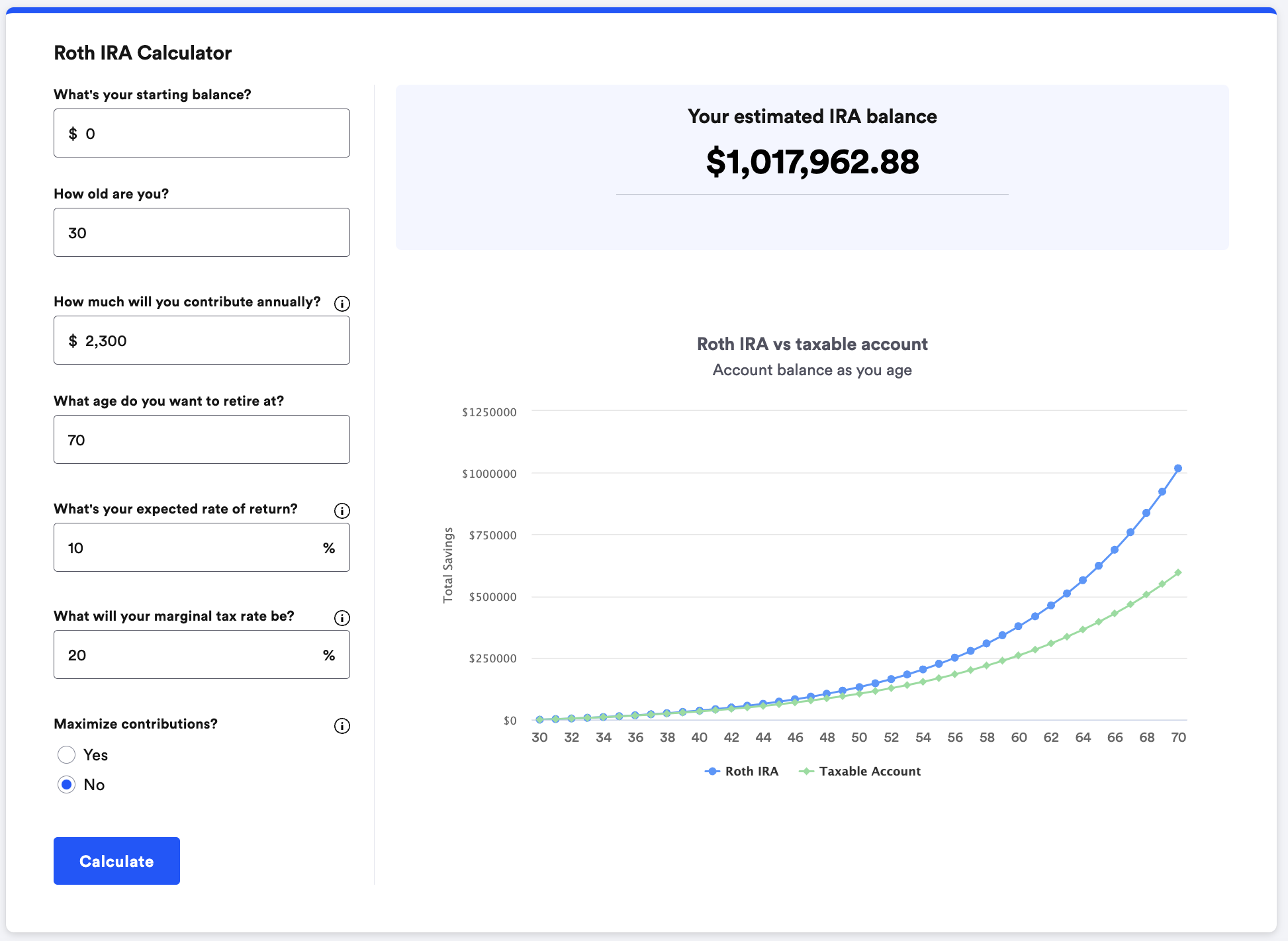

Graph and Image Provided by https://www.bankrate.com/retirement/roth-ira-plan-calculator/

Amazing, right? What’s the catch you say? Is it hard to do? Will I have to pay extra taxes? Are there fees and expenses? Good Questions!

The Answers; No, No, and No (just make sure you sign up for electronic statements from Vanguard*). This money grows tax-free, so when you withdraw it you owe nothing on all the gains.

Setting up a ROTH IRA via Vanguard or another similar institution like Fidelity takes an average of 5 – 10 minutes. Open Account Here

Reader: OK, Ryan, I am not 21 years old anymore, I am 30 years old what now!?

Me: The good news is you can likely afford much more than when you were 21, although you will not have the very important time in the market on your side, you can make up for it with increased contributions.

If you can afford $50 a week or $200 a month you are on your way to an easy million!

Reader: I hate to admit it but I am 40 and am just getting around to setting all this up, I lived in a practice room shutting myself off to #adulting.

Me: No Problem, we got you covered!

Look at that, you still get to sip sparkling water on the beach in your luxurious retirement! Thanks to the IRS Catch up contribution of an extra $1,000 after the age of 50, we were able to catch you up, plus some extra!

How much a month do you need to to save to put this plan into action? $500 a month or $125 a week. This is a number that is doable for most individuals or couples in their 40’s, but if you cannot hit this exact amount, that is totally fine, just consider doing as much as you can.

**The Most Important Thing**

Pay yourself first and Automate your contribution. Here is how

I have found that when I set up automatic investments I don’t “feel it” at all. Over the years I have slowly upped my savings amount a little bit every year until one hits the limit for the respective account type. The IRS limit for ROTH accounts in 2024 is $7000 or $583 a month.

I hope you have gotten some inspiration to open up and automate your ROTH account today! Your future-self thanks you in advance.

Please feel free to reach out with questions, comments, or other topics you would like to me cover in the coming weeks!

– Ryan

*The ROTH IRA fee from Vanguard is $20 a year, but is completely waived if you do electronic statements.